Let’s first turn to the obvious negatives. The Trump idea is an admission that he and pretty much everyone are unserious about addressing the housing unaffordability problem because too many powerful players benefit from it. The most obvious remedy is to build more middle/lower middle class residences in high cost areas. But right away, that runs hard into NIMBYism: all those well off with their tony houses don’t want the servant classes or even dull normals living nearby and possibly harming their property prices.

… the popular freely-refinancable (as in no prepayment penalty) 30 year fixed rate mortgage is a very unnatural product and is found in comparatively few advanced. economies. On paper, it puts the interest rate risk on the lender. If rates drop, borrowers refinance, taking the loan away from creditors just when taking the risk of longer-dated loans is paying off. There are many ways to better share the interest rate risk, such as barring refis for the first five to seven years of a mortgage, or having interest rates float subject to a floor and ceiling. I had that sort of product in the early 1980s and was very happy with it. You can pencil out what your worst-case mortgage costs might be and benefit with no expenditure of effort if interest rates fall.

So why is this supposedly borrower-favoring feature, of the “freely refinancable” fixed rate mortgage, actually not good for borrowers? Because that option is NOT free! Not only do borrowers pay fees when they refinanace, but lenders have succeeded in structuring refis so that roughly 2/3 of the economic benefit of the refi is captured by financiers, not by the homeowner.

A related bad feature of the refinancable 30 year mortgage is that it increases systemic risk. Mortgage guarantors Fannie and Freddie have to hedge the refi risk. That hedging is pro-cyclical on a systemically disrupting scale.

…

50 year mortgages, compared to a 30 year obligation have more of their payments over their life in interest. That means in a refi more total interest savings. That means even more in fee extraction by middlemen! More critically, it also means much greater pro-cyclical hedging action, and thus an even bigger increase in systemic risk, assuming that there actually was consumer receptivity to this bad idea…

Yeah but I’ll pay $200 less a month! /s

For only 240 extra months!

As long as we can keep this ponzi scheme going it doesn’t matter you’ll make it back.

While I fully agree this doesn’t solve any affordability concerns, for those with no affordability concerns that $200/month is better served in a portfolio, which will inevitably have a higher return than a secured interest rate. This does help, but it only helps people with no issues with affording a home in the first place, and can use the system to make further gains (albeit fairly minor).

Just think about how many extra streaming services I can pay for now!

Yeah and your $800/mo new car with leather seats gets 6 miles per gallon more than the paid off base model. ExxonMobile is practically paying you now!

A 50 year mortgage is just renting with extra steps and additional responsibility.

When you rent the landlord has to pay taxes and maintainance.

So it’s likely the middlemen corps that have told Trump to attempt to implement this, isn’t it?

And so the gap between the classes widens again. 1.2m in interest on a 420k asset, paid over your entire adult life. Imagine being stuck paying >2000$/month for life to a bank, BUT with the additional costs of maintenance & probably an HOA & rising property taxes. At that point, renting is the only option, but the prices of that will rise too. So GG capitalism, it’s time to tape leaves to a tent and live in the middle of a roundabout with your 4 cats and a handgun

I’m not sure why this is a better argument against a 50 year mortgage than against 15 or 30 year mortgages. The author does say that 50 years gives more opportunities to refinance, but many people who buy homes don’t intend to live there 50, 30, or even 15 years. For these people, the only thing that matters is the monthly payment and the choice of a lower payment but with more of that payment going towards interest can be a rational one.

With an interest rate of 6.5% you have a doubling time of roughly 10 years. So over 50 years it’s a huge difference.

WTF is with this articles shit talking of fixed rate rate mortgages that let you refinance without penalty? That is literally the only half-way consumer friendly thing we even have in our current scheme. They talk about how in the early 80s (one of the worst times ever to get a mortgage) they had a way shittier mortgage and how “happy” they were with it. That’s bullshit and their reasoning doesn’t pass muster. I suspect this was written by some finance ghoul trying to astroturf getting people onto more awful systems.

They make it sound like lenders game the system to make the fixed rate loans not super beneficial (refinance costs/etc.). I have no idea how true that is, but even if it is, having a fixed amount you owe each month is so much easier for the everyday person.

I can’t imagine having a variable rate loan and then finding out due to the Fed raising rates that I know owe another couple hundred per month.

Been there and it sucks, I have also been stuck in a mortgage that had restrictions on refinancing and it also sucked. Anyone thinking they wouldn’t get gouged just as hard after giving up their fixed rate and refi ability are delusional or in on the grift.

Yeah, I was thinking that too. Of course they’re going to try to get the most money out of you, it feels like fixed rate mortgages though at least give the buyer some leverage.

I can’t imagine having a variable rate loan and then finding out due to the Fed raising rates that I know owe another couple hundred per month.

Mortgage products like this were in the causal mixture for the 2008 crisis. People could own three or four different homes, maximally leveraged, and then get ARMs on them. This house of cards “works” as long as the interest rate stays low and prices go up. Then there was a rate adjustment upwards and all hell broke loose.

Other countries don’t have 30 year fixed like we do so there are systems to deal with this. Usually there’s no set repayment timeline, but rate is fixed for some period. Then it goes variable, or you negotiate a new fixed rate for another 5 or 10 years or whatever. The amount you contribute after interest is up to you and determines your payoff time.

Explain the 50 year mortgage in layman’s, I mean idiot term for me please.

It’s beyond bad, it’s outright dumb as fuck.

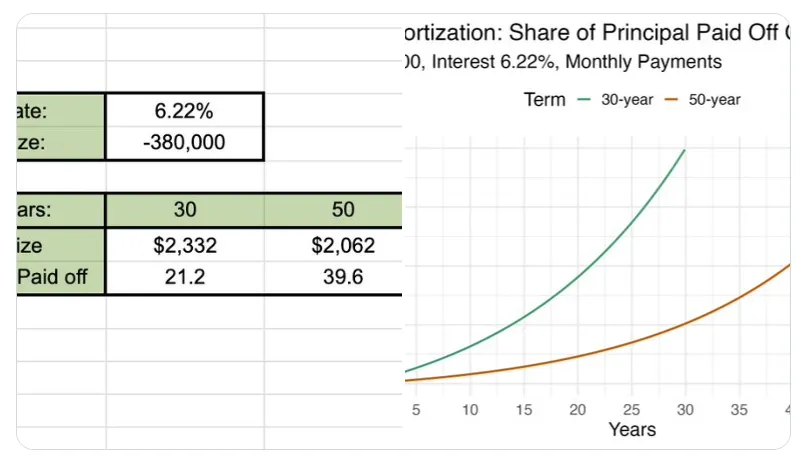

As it stands, a 30yr mortgage at current interest rates means that you end up paying ~$1.20 in interest for every $1 borrowed.

A 50yr mortgage at current interest rates would have you pay $2.50 in interest for every $1 borrowed.

You would end up literally paying 3.5x the value of the mortgage - it’s outright criminal.

I was reading up on it. Apparently a fannymae chairman came up with it and Trump went with it. What a fucking joke, a bank responsible for the last financial crisis is running the govt now.

Thanks for breaking it down. The articles were saying double the mortgage and it seemed unbelievable. I think you usually pay the interest first on a mortgage also.

A portion of the payment goes to interest and a portion goes to the principal. The first payment is almost all interest and a tiny bit of principal. The last is almost all principal and a tiny bit of interest.

As you reduce the principal you are paying less in interest each payment and more principal.

One way to greatly reduce your loan time is to pay one extra payment each year year having it go all to principal. That can cut 4-6 years of a 30 year mortgage.

Put simply, it decreases your monthly payments but extends how long you will make those payments. So compared to a 30 year mortgage, you’ll pay something like 85% as much per month on your mortgage (15% less), but for 167% as long (20 years longer)

0.85 × 1.67 = 1.42, meaning you will end up paying 42% more for the same house in the end. That means you will just about double, give or take, the interest paid to your loaner. And the house wont be yours until 50 years is up, meaning you paid 42% more for a 20 year older house, by the time you could sell it for full equity (i.e. didnt have to pay anything to the loaner). And that is IF you even live for the full 50 year, which most people wont. The average first time home buyer now is already in their 30s, meaning they will be in their 80s by the end of their mortgage. 71-72 is average life expectancy. So instead of inheriting your home, you kids will more than likely inherit an ongoing mortgage, or lose the house to foreclosure.

The simple fact of that matter is that homes are too fucking expensive. Yes, a 50 year mortgage will drop your monthly payments by a significant margin (maybe 15ish percent) increasing affordability for the long term. However, this will only serve to prop up already inflated housing prices. The problems with that should be readily apparent.

A) if your house is twice as expensive as it should be, your payments will be twice as expensive at it should be. Thanks for the extra 15% off a month, but that still doesn’t get payments to anywhere near as affordable as it would be if housing was more available and, thus, cheaper. It would be better to forgo that 15% monthly payment decrease by extending your mortgage (and massively increasing interest), and instead see a 10% market price decrease and keep your 30 year mortgage and end up still paying less overall.

B) The biggest hurdle for any prospective home buyer is the initial hurdle, the down payment. You have to be able to pay for your current housing (be it mortgage or rent or whatever) and other necessities while also setting aside money on the order of tens of thousands to afford just the down payment on a house to even qualify for the loan. For even a modest home in my area, the lowest on market currently is asking ~175,000 for under 900 sq ft. 20% down for that would be 35k that you need to have saved before even considering buying the cheapest home in town. Extending the mortgage not only doesnt help you on this, it actually makes this hurdle worse. It makes mortgages easier to get for current home owner, in turn proping up the housing prices making it prohibitively expensive for renters and first time home buyers that dont have the equity in property to sell off to cover this down payment. And as the housing prices continue to inflate that 35k goal post just keeps moving further away every year while your money is sunk into your landlord’s pocket, who also increases rent as the market increases.

Prices needed to come down. Rents need to stop rising. And corporate real-estate investors need to be outlawed, or at least heavily regulated to prevent this absurd inflation. First time home buyers should be the first priority in real-estate and housing policies, not the last. We used to actively support them, but now we are more worried about boomers’ resale value and squeezing renters for every dime. It has to stop. Build more housing, more homes, more dense housing. Make competition for the landlords and give first time home buyers every advantage over investment buyers, particularly corporate investment buyers. Fund it with the American tax dollar and see the middle class rise back up. It’s really that easy, but they just wont do it becuase Daddy Warbucks wouldn’t like it.

Yes, a 50 year mortgage will drop your monthly payments by a significant margin (maybe 15ish percent) increasing affordability for the long term.

The actual numbers will likely not bear that out. Some back of the envelope math in this article and others has the payments dropping as little as $150 or $200 on a $2000 mortgage.

The problem is that rates for longer mortgages are naturally going to be higher as they are today. Most of the “gain” of stretching out the loan is eaten up by interest.

What does never seem to catch anyone’s eye though in general is…you can pay more than the minimum on your mortgage just like any other type of debt. If these products were available, I’d be slightly tempted to use one to lower my required monthly payments slightly while I saved up the principle to repay the loan in full.

There should be a progressive tax on anyone that owns a home but doesn’t live there. First home is nominal tax. Second home is double that. Third is quadruple. That’d fix housing and rent prices overnight.

And before anyone asks, yes same with apartment complexes. If the owner is forced to live in the complex, there’s an excellent incentive to keep it clean and maintained. And I’m specifically talking people, if a corporation owns a complex the top shareholder needs to be living there.

home is nominal tax. Second home is double that. Third is quadruple. That’d fix housing and rent prices overnight.

I dont think that would fix rents necessarily unless the taxes were particularly prohibitively. They’d just be incentivized and have an excuse to raise taxes more, seems like.

Financial slavery is just another name for slavery.

No one in the us ever looks at how things work in other countries, right?

While we don’t have the exact same mortgages setup in the EU, it’s not in any way uncommon for our house loans to not be realistically paid down during one’s life time. Yeah, we indeed refer to it as renting from the banks.

If the regressive dumbasses in this country don’t succeed in their (apparent) project of completely ruining science and medicine in this country, I would not be surprised to see the average lifespan/healthspan go up.

Even so, I still think 50 year mortgages are rather stupid. But with dipshits running things, it would not be surprising to see the combination of the worst kind of outcomes even in the face of breakthroughs in age extension/reversal - people still being forced into retirement early, but coming up with schemes like 50 year mortgages at the same time…barf.